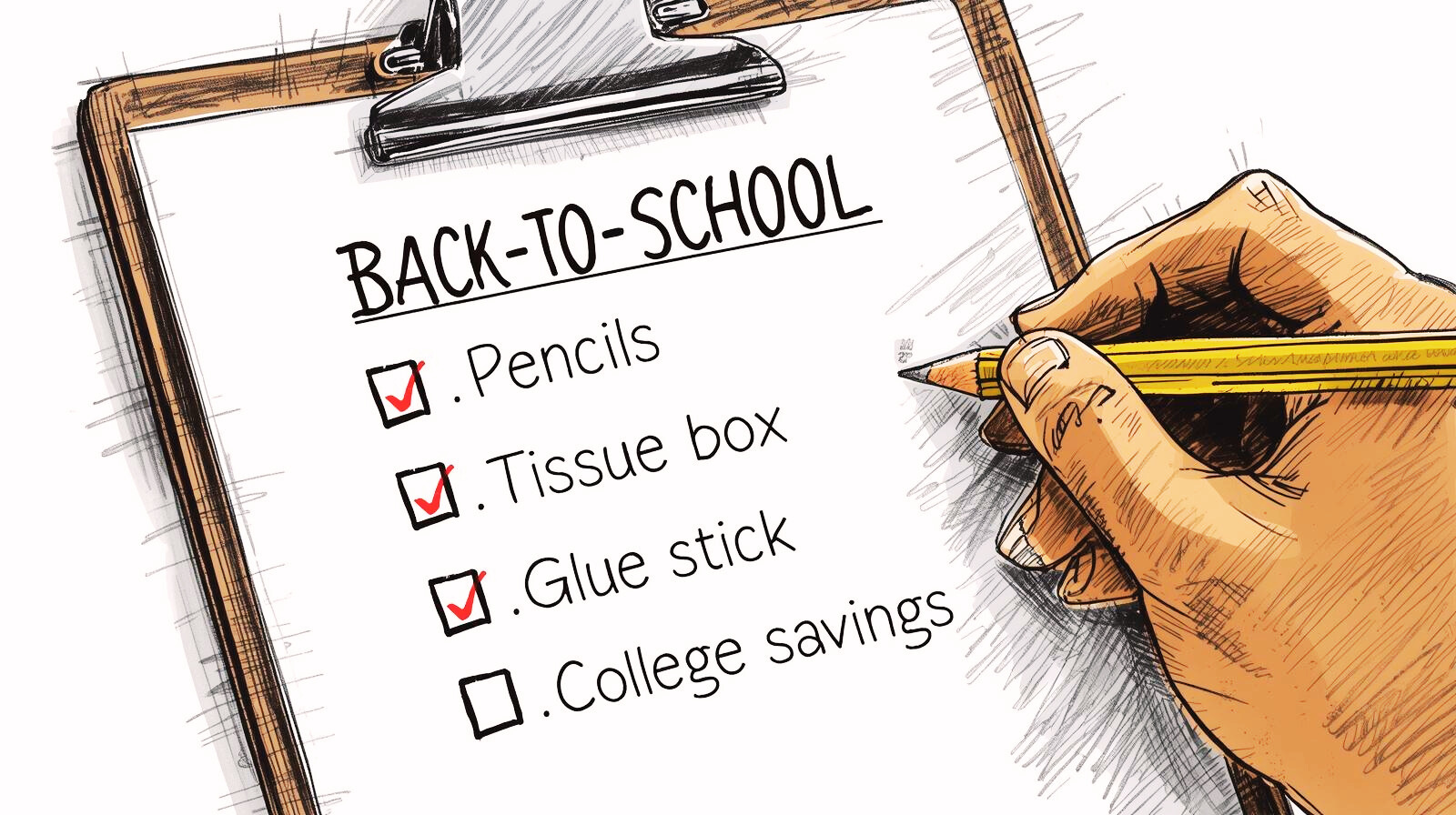

The Future Costs More Than Pencils

Every August, your child’s school hands you a list: pencils, notebooks, markers, and glue sticks. You dutifully check the boxes, filling carts with the supplies your child needs for the upcoming school year.

But there’s something on that list the school won’t account for, the plans for your growing child to be able to afford the next stage of life after high school. Although most people think saving for college is all about timing, it’s really about getting started. Waiting for the perfect time is a trap, and the cost of doing nothing could set your child back for the rest of their life.

While today’s supply list might set you back a couple of hundred dollars, tomorrow’s education costs could stretch into the tens of thousands. Many years from now, what will be waiting on the other side of your child’s acceptance letter, opportunity, or debt?

The Cost of Doing Nothing

For the 2023–24 school year, the average tuition and fees at a public, four-year in-state university were $10,940. At a private college, tuition alone averaged $39,400 per year. Add in room, board, books, and transportation, and the annual cost can climb well above $55,000.

Community colleges remain more affordable, but even they average close to $4,000 per year, and like everything else, those prices are going up. Historically, tuition has risen about 5–6% annually. If that continues, by the time today’s toddlers are ready for higher education, a four-year private program could easily top $200,000.

Without scholarships, the result can be debt that follows them for years.

Right now, 43 million Americans are burdened with student loans, with balances averaging more than $37,000. Many will spend decades paying them off, sacrificing home ownership, retirement savings, and even family plans just to stay afloat. It’s a burden that shapes lives long after graduation. But luckily, it doesn’t have to be this way.

But here’s the thing: it doesn’t have to be this way.

Why 529 Plans Deserve a Spot on Your Back-to-School List

When parents think about saving for education, the question often isn’t why but how. That’s where a 529 plan comes in. It’s one of the most flexible, tax-friendly ways to set money aside for your child’s future schooling—whether that means college, trade school, or another qualified program.

The biggest advantage is growth. Money invested in a 529 grows tax-free, and when it’s used for qualified education expenses, you don’t pay federal taxes on the withdrawals either. Over 10, 15, or 18 years, that tax break alone can add thousands of dollars to your child’s account.

Another key benefit is that anyone can contribute. Grandparents, relatives, and even close family friends can add to your child’s plan. This makes it more than just a parent’s effort, it can become a family project. Instead of one more toy that gets forgotten in a month, loved ones can give a gift that lasts decades.

And unlike savings accounts that just sit and earn little interest, most 529s allow you to invest in age-based portfolios and types of portfolios that cater to long-term growth. That means the money has more potential to cultivate while your child is young, and then gradually shifts into safer investments as they get closer to graduation.

In other words, a 529 plan takes advantage of both time and smart investing. Even small contributions now can lead to meaningful freedom later.

Why Time Matters More Than Timing

Many parents tell me, “We’ll start saving when things settle down.” But if there’s one lesson I’ve learned, and one Morgan Housel emphasizes in The Psychology of Money is that waiting for the perfect time is a trap.

There’s always another expense, another reason to hold off. But wealth isn’t built by timing the market or waiting until you have “enough” to start. It’s built by habits, consistency, and letting time do the heavy lifting.

Education savings work the same way. It’s not about waiting until you can contribute hundreds each month. It’s about starting with something. Create a routine where even $25 or $50 at the end of the month becomes as easy as paying another bill, instead you’re paying today for a potential lesser headache in the future. Over the years, those small steps compound into something big.

Meet Annie

Take the story of Annie Boyd Sowell, a mom who wrote about her experience in Business Insider. When her son was a baby, she and her husband decided to open a 529 savings plan. At the time, money was tight. They had a mortgage, monthly bills, and all the costs of raising a child.

Instead of waiting until their finances felt perfect, they contributed what they could. Sometimes as little as $25 each month, and other times as much as $50. Over time, it added up. More importantly, the habit became non-negotiable.

Annie admitted the peace of mind mattered just as much as the money. Even in months when the budget was stretched, she knew they were building something real for their son’s future.

Her story is proof that it’s not about doing everything perfectly. It’s about doing something consistently. The most underrated force in finance is consistency.

Beyond School: A Flexible Future

Now, let’s pause here. Because it’s important to say: life after high school isn’t one-size-fits-all.

Some kids will thrive in a university system while others will find their calling in trade schools, apprenticeships, or vocational programs. Some may even start businesses right out of high school.

The good news is that many education savings plans, like 529s, aren’t limited to traditional colleges. They can also be used for trade schools and qualified training programs. You’re investing in peace of mind at the very least with a degree of flexibility. But what happens if your child doesn’t use the funds at all? In many cases, you can transfer the savings to another child, or even to yourself if you want to continue your own education. Just make sure to check with your Financial Coach or Planner before you make this move.

The point isn’t to lock your child in a single path. It’s to give them options—and to make sure debt doesn’t close doors before they even get to choose.

Just Be Aware of Downsides

All this good information doesn’t come without its drawbacks. Even a well-informed parent can feel overwhelmed by starting a task that seems so large. First, let’s start with the different options in college savings plans.

To save time, I’ll stick to the traditional 529 Plan, Uniform Gifts to Minors Act (UGMA), and the old school savings bond. With a 529 Plan, you’ll need to be aware that almost every State has its own plan, with some States giving tax deductions while others don’t. The 529 Plan has a contribution limit of up to $15,000, but it must be used for education if you don’t want to be taxed on withdrawals.

UGMA plans have no contribution limit and could lower the taxes of the contributor. Unfortunately, beneficiaries will be taxed when funds are withdrawn. Savings bonds are low risk but also have low returns and penalties for early redemption.

The best approach is to do a little research to see what is available to you and what best benefits your situation. Remember, just like college, saving for it is not a one-size-fits-all solution.

Building Momentum Through Habits

Most parents get stuck in the mindset that saving has to be hard, but saving for the future works best when it’s simple and automatic.

Think about how you already handle everyday expenses. You don’t sit down and calculate each grocery item before you buy it. Instead, you make the trip every week because it’s part of your routine. Saving can work the same way.

Here are a few habits that create momentum:

Automate contributions. Set up a small, automatic transfer each month into your child’s education savings. When the money moves without you having to think about it, saving becomes a background habit like paying a bill you don’t miss.

Link savings to milestones. Birthdays, holidays, and even the start of each school year can be natural checkpoints for contributions. Starting this habit at the beginning of the school year will give you a point to mark your progress each year. If you want to make it interesting, ask grandparents and relatives to contribute a monthly amount they won’t miss or really think too much about.

Round up small amounts. Apps and bank tools can round up everyday purchases and direct the spare change into savings. Bank of America and Acorn are well-known companies with this savings feature built into some products.

Celebrate progress. Occasionally, check the balance with your child without focusing on the size of the number. Teach them that saving isn’t about instant results, but rather about building something steady. This turns the habit into a family value.

In The Psychology of Money, Housel makes the point that financial success is more about behavior than intelligence. The smartest people in the world often stumble with money because they don’t stick to good habits. Meanwhile, ordinary families who save steadily, without overthinking, often end up in a far stronger position.

When you focus on habits rather than hurdles, saving no longer feels overwhelming. It becomes part of life. Over time, that momentum does more than you’d ever expect.

The Back-to-School Challenge

Here’s my challenge to you. Alongside the notebooks and sneakers, take one step toward funding their future. Maybe that’s opening an education savings account. Maybe it’s setting up an automatic transfer for a small amount each month. Or maybe it’s talking to grandparents about contributing as a gift for birthdays and holidays.

Because years from now, when your child opens that acceptance letter or signs up for an apprenticeship, you’ll know you gave them something far more valuable than supplies. You gave them freedom.